One of the area’s largest developers has ties to what appears to be a coordinated property‑transfer pattern, with records linking Glacier Bank, now under scrutiny in Montana’s Flathead Valley.

As Dennis Thornton’s nearly two‑decade effort to restore full control of his property continues through the courts, his team has increasingly focused on reconstructing the record itself, assembling timelines, filings, and land transactions that tell a far more troubling story than any single court ruling ever could.

This narrative is supported by court filings, sworn testimony, expert‑witness reports, and the public record. Although the Thornton case has become increasingly complicated, this exposé strips away that complexity to present the facts in plain terms for all Montanans.

To fully grasp the breadth and depth of what Thornton has endured, this story must begin at the outset, in 2008, when Glacier Bank held the mortgage on Thornton’s disputed Somers property. At that time, Whitefish attorney Sean Frampton served on Glacier Bank’s Board of Directors while also acting as outside counsel for Whitefish Credit Union. Frampton’s name will appear frequently as this narrative unfolds.

According to expert witness Gerald Fritts, Glacier Bank originally held Thorco’s pre‑development loan and, not Thornton, submitted a $7.2 million construction and refinance request to Whitefish Credit Union on Thorco’s behalf. Whitefish Credit Union ultimately funded only $3.36 million, with the first disbursement used to pay off Glacier Bank, effectively transferring the loan while leaving the larger development plan partially unfunded.

As this transaction unfolded, Thornton’s loan was effectively transferred from Glacier Bank, where Frampton served on the board, to Whitefish Credit Union (WCU), which retained Frampton as outside counsel, a role that would become increasingly consequential for WCU as events progressed.

After the mortgage was transferred and Glacier Bank was paid off, Whitefish Credit Union moved quickly in a manner that later testimony would cast into question. In sworn deposition testimony cited by expert witness Gerald Fritts, loan officer Randy Cogdill admitted that shortly after Thorco entered into the 2009 loan with WCU, he was showing the disputed property to a Missoula developer for a possible sale, despite WCU not owning the land.

In the years following the 2009 transfer of Thorco’s loan to Whitefish Credit Union, the development steadily advanced while the promised structure of financing unraveled. Thorco completed substantial value‑added work on the Somers property, including roads and infrastructure, much of it independently funded or bonded, while repeatedly seeking the second phase of financing that had been contemplated as the repayment mechanism for the original loan.

According to expert witness Gerald Fritts, Whitefish Credit Union neither formally rejected the original construction request nor notified Thorco that refinancing would no longer be available, instead relying on significantly reduced appraisals that ignored completed improvements and intended use.

As refinancing and subordination requests stalled or were denied, the relationship deteriorated into foreclosure proceedings, undertaken without a completed workout process, even as Whitefish Credit Union personnel explored interest from outside developers before acquiring any ownership interest in the land.

One only needs to examine a summary of the report issued by former senior official and director at the National Credit Union Administration, Allen Carver, to gain insight as to what was really at play behind the scenes at WCU.

______

Former NCUA director Alan Carver concluded that Whitefish Credit Union was under regulatory pressure and effectively barred from making new development loans during the period when Thornton was expecting the second phase of construction financing. According to Carver’s findings, the credit union failed to notify its member borrowers of this restriction, leaving them unaware that promised refinancing would not be forthcoming. The Carver report further determined that, rather than disclosing its regulatory limitations and working with borrowers, Whitefish Credit Union shifted toward foreclosure activity, a departure from standard credit union practices and regulatory expectations.

In short, Whitefish Credit Union had the option to work with Thornton, who maintained an 800‑plus credit rating and a twenty‑million‑dollar bonding line, but instead chose to pursue foreclosure actions against him.

Fritts further reports that throughout this period, WCU personnel were in contact with at least one outside developer regarding the possible sale or takeover of the property, even though WCU had not yet acquired ownership through foreclosure. He characterizes this activity as inconsistent with standard lending practice and indicative of intent that preceded the foreclosure action.

After Whitefish Credit Union initiated foreclosure proceedings in 2012, the case moved into prolonged litigation marked by counterclaims, discovery disputes, and competing appraisals. Thornton challenged the foreclosure while continuing to seek refinancing and other avenues to resolve the loan through payment rather than surrender of the property, pointing to completed development work and unmet lending commitments.

Over the next several years, depositions and discovery revealed internal communications and third‑party interest in the land, even though Whitefish Credit Union had not acquired ownership. In early 2016, while Thornton’s counterclaims remained unresolved, Whitefish Credit Union obtained a foreclosure judgment that was promptly challenged. Before any sale took place, the parties jointly moved to vacate that judgment, and in 2016 the court granted the motion and dismissed the case with prejudice, bringing the foreclosure action to an end… or so Thornton thought.

Judge Dan Wilson Violates Montana Code?

In 2018, the case took a decisive turn when Eleventh Judicial District Judge Dan Wilson issued rulings that effectively resurrected Whitefish Credit Union’s foreclosure position. Despite the fact that the 2016 foreclosure judgment had been vacated and the case dismissed with prejudice, Wilson ruled that the underlying debt remained owed and enforceable, relying in part on the very foreclosure judgment that had been set aside.

Those rulings allowed Whitefish Credit Union to proceed as if the prior adjudication had never occurred, reshaping the dispute and setting the stage for the events that followed. Wilson ruled in a manner that, in Thornton’s view and according to the statutes listed below, conflicts with Montana law:

MCA 71-1-222

One action rule. There is only one action for recovery of a debt or enforcement of a right secured by a mortgage. Once that action is taken and resolved, no further action on the same debt is permitted.

MCA 25-20-41 (Rule 41, Montana Rules of Civil Procedure)

A dismissal with prejudice operates as an adjudication on the merits and permanently terminates the action unless the order states otherwise.

MCA 25-9-301

Judgments create liens only while they are valid and enforceable. A vacated judgment cannot serve as the basis for a continuing lien.

MCA 71-3-131

When a lien or claim is satisfied or found invalid by final order or judgment, the creditor must acknowledge satisfaction and release the lien of record.

MCA 71-1-105

A mortgage does not entitle the mortgagee to possession of the property without foreclosure and sale.

MCA 71-1-101 and MCA 71-1-103

A mortgage is a security instrument only and does not convey title or ownership.

Inquiring minds would like to know how Wilson, who is running for the Montana Supreme Court, would move forward with his 2018 decision in violation of the above-listed Montana Code. One would naturally ask if Wilson just didn’t know, or did he know and rule against Thornton anyways? Either interpretation raises serious questions that voters may wish to consider as Wilson seeks elevation to Montana’s highest court.

Following Judge Dan Wilson’s 2018 ruling, which treated Whitefish Credit Union’s extinguished foreclosure debt as if it remained valid, the dispute entered a new phase. Despite the prior vacatur and dismissal with prejudice in 2016, Whitefish Credit Union continued to assert an enforceable debt in subsequent proceedings, relying on filings and affidavits that restated amounts previously nullified by court order.

According to Fritts, this posture allowed the continued use of security instruments and mortgage documents as though a lawful foreclosure path still existed, even though no valid judgment supported that position. The effect of the 2018 ruling was to reopen, in practical terms, a foreclosure that had already been terminated, reshaping the parties’ legal positions and enabling further action against the property.

As mentioned earlier, Whitefish attorney Sean Frampton has played a key role in the Thornton property dispute from the beginning. According to a series of sworn affidavits by private investigator Katherine Wilson, the breakdown in the Thorco title chain began when deeds executed during post‑litigation settlement discussions were not delivered to a licensed title or escrow company for immediate, lawful processing. Instead, those deeds were retained by Whitefish Credit Union’s counsel, Sean Frampton, who was not licensed as a Montana title or escrow officer.

Wilson’s investigation found that the deeds were kept outside any formal escrow, then later surfaced in the public record disconnected from a valid foreclosure, closing, or contemporaneous satisfaction of the mortgage. Interviews with personnel at Title Financial Specialty Services confirmed that the deeds did not pass through standard escrow channels when executed, creating a gap that allowed security instruments to later be used as apparent conveyances.

In Kathy Wilson’s analysis, the custody and delayed recording of deeds created the conditions for subsequent title transfers and ownership claims that should not have been legally possible following the 2016 dismissal of the foreclosure with prejudice. Read more by clicking here

The Montana Supreme Court Violates Montana Code?

Between 2019 and 2021, the Montana Supreme Court issued two memorandum opinions connected to the fallout from these proceedings. While neither opinion was designated for publication or precedential value, both had the effect of leaving Judge Wilson’s rulings intact.

As presented in the Fritts report, the Supreme Court did not disturb the underlying assumption that the debt survived the 2016 dismissal with prejudice, even though that dismissal was final on its face.

By 2021, the combined effect of the district court rulings and the Supreme Court’s noncitable affirmances was that actions taken against the property were treated as legally operative, notwithstanding the earlier adjudication that had extinguished the foreclosure and the debt itself.

Courts, including the Montana Supreme Court, are bound by the Montana Code Annotated and the Montana Constitution. They do not get an exemption. What follows is not an accusation of criminality, but a list of Montana statutes and procedural law that are implicated when the Supreme Court affirms or relies on an extinguished judgment or debt:

MCA 71‑1‑222

One‑action rule. There is only one action for recovery of a debt or enforcement of a right secured by a mortgage. Once that action is taken and resolved, no further action on the same debt is permitted.

MCA 25‑20‑41 (Rule 41, Montana Rules of Civil Procedure)

A dismissal with prejudice operates as an adjudication on the merits and permanently terminates the action unless the order states otherwise.

MCA 25‑9‑301

Judgments create liens only while they are valid and enforceable. A vacated judgment cannot serve as the basis for a lien or further enforcement.

MCA 71‑3‑131

When a lien or claim is satisfied or found invalid by final order or judgment, the creditor must acknowledge satisfaction and release the lien of record.

MCA 71‑1‑101 and MCA 71‑1‑103

A mortgage is a security instrument only and does not convey title or ownership absent a valid foreclosure.

MCA 71‑1‑105

A mortgagee is not entitled to possession of the property without foreclosure and sale.

Montana Constitution, Article II, Section 17

No person may be deprived of property without due process of law, which requires enforcement actions to be grounded in a valid judgment.

Mo Somers

As the courts left Judge Wilson’s 2018 ruling intact, concerns about Whitefish Credit Union’s conduct were already shifting beyond the judiciary and into the legislative arena. Borrower complaints reached the Montana Legislature’s Bank Oversight Committee, where testimony by Melanie Hall placed the credit union’s foreclosure practices under direct scrutiny by state regulators and lawmakers.

That testimony marked a turning point, signaling that questions about the legitimacy of Whitefish Credit Union’s actions were no longer confined to court filings alone. It was in the wake of that oversight process, and after the judicial and regulatory paths had effectively stalled, that Mo Somers, LLC first appeared in the record, not as a participant in the original lending or foreclosure, but as a new entity positioned to receive title through special warranty deeds tied to the same disputed paper trail.

Mo Somers, LLC entered the record not as a party to the original loan, development, or foreclosure, but as a new entity that appeared only after the courts and regulators had failed to resolve the underlying dispute. The company surfaced through a series of special warranty deeds tied to the same contested documents and extinguished debt that had already been questioned in court and before the Legislature.

Nothing in the record places Mo Somers in the early history of Thorco’s property or in the lending relationship itself. Instead, its appearance marks a shift from litigation to paper transfers, with Mo Somers positioned as an intermediate title holder whose claimed interest depended entirely on post‑dismissal instruments rather than a valid foreclosure or clear satisfaction of the mortgage.

The manner in which Mo Somers acquired its claimed interest draws renewed attention to the handling of the underlying documents themselves. The deeds placing Mo Somers into the chain of title did not emerge from a conventional escrow closing or a completed foreclosure, but from a record built on delayed and selectively deployed instruments.

Those deeds traced back to documents that had been executed years earlier, outside normal title practice, and surfaced only after litigation and oversight efforts had run their course. This paper‑first approach to ownership, untethered from a contemporaneous sale or satisfaction of the mortgage, reopened unresolved questions about who controlled the documents, when they were released into the public record, and for what purpose.

It is against that backdrop that Sean Frampton reappears in the record, again connected not to a courtroom ruling, but to the movement and correction of the paperwork itself.

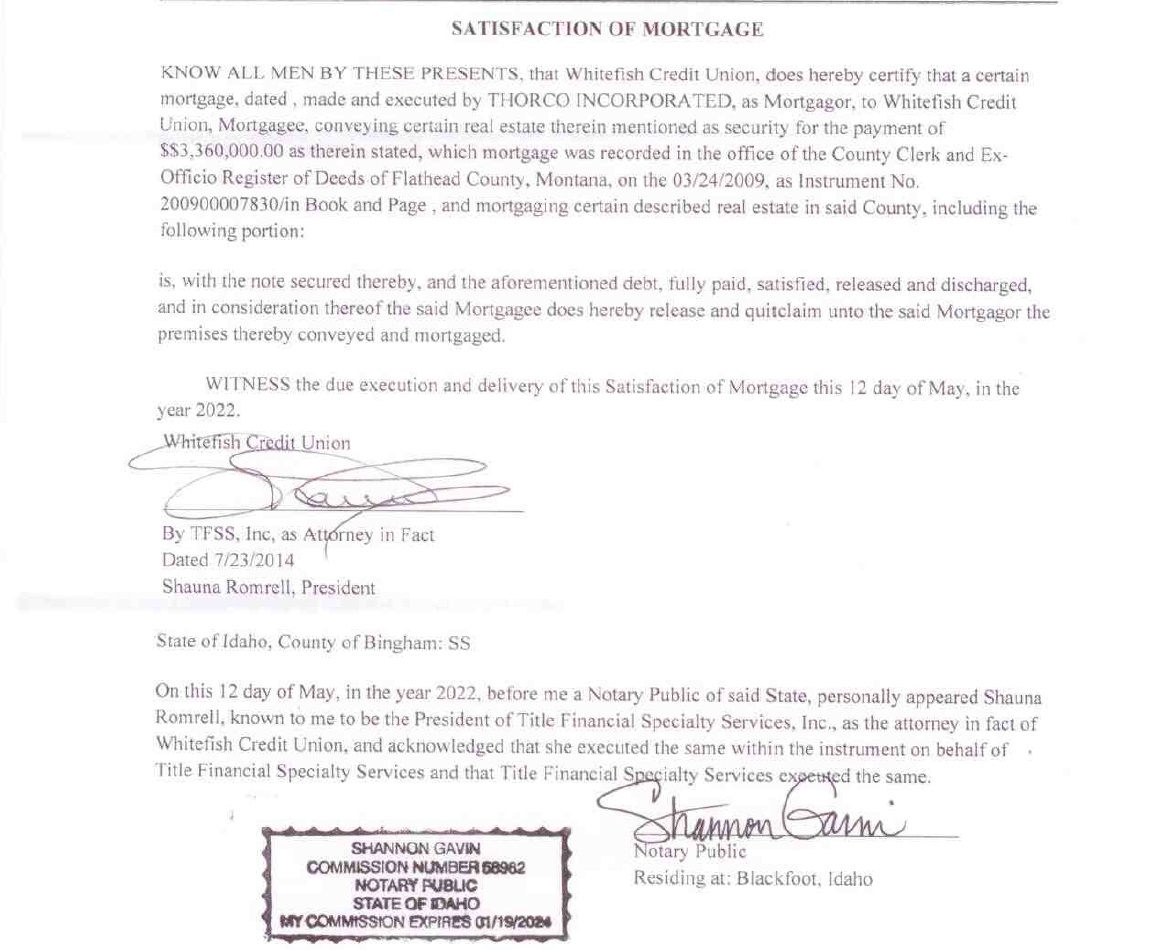

Before any so‑called correction appeared in the public record, Whitefish Credit Union had already taken affirmative steps that should have ended the matter altogether. In May 2022, its agents executed and recorded a Satisfaction of Mortgage and an accompanying quitclaim deed, documents that on their face acknowledged the extinguishment of the lien and disclaimed any remaining interest in the Thorco property.

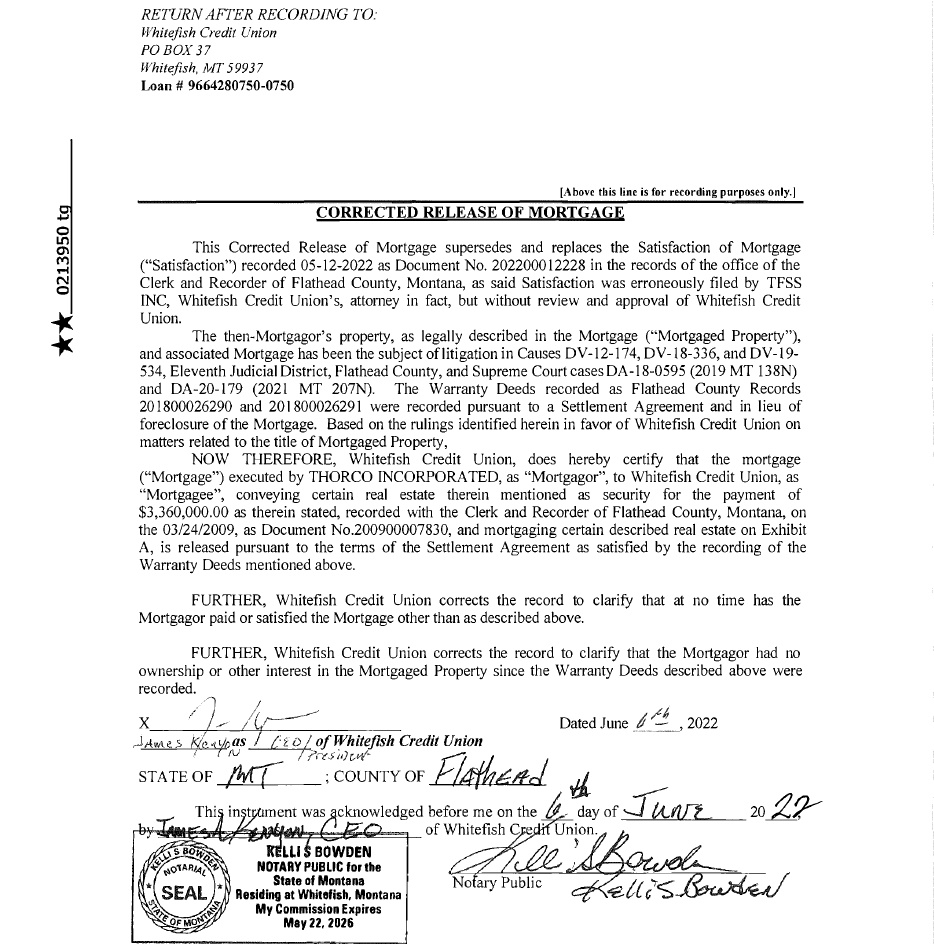

Those filings were not provisional, conditional, or subject to further judicial action. They were recorded instruments, intended to clear title and close the chapter opened years earlier by an already dismissed foreclosure. It was only after these acknowledgments had been placed of record, and after Mo Somers had briefly occupied the chain of title through special warranty deeds built on disputed paper, that Whitefish Credit Union returned to the recorder’s office with a “Corrected Release of Mortgage,” purporting to revise what had already been satisfied and disclaimed.

By that point, the issue was no longer clerical error, but the resurrection of an interest that the credit union itself had formally laid to rest. That context matters because the Satisfaction of Mortgage and quitclaim were not filed in ignorance, delay, or without notice.

In later filings, Whitefish Credit Union’s counsel, Sean Frampton, acknowledged that he was contacted by Travis Ahner and informed of the quitclaim shortly after it was issued. Despite that direct notice, and just twenty‑five days later, Whitefish Credit Union returned to the recorder’s office with a document titled “Corrected Release of Mortgage,” filed on June 6, 2022 by CEO James Kenyon.

The filing was not accompanied by a new court order, a reopened foreclosure, or any intervening judicial development. Nor did it correct a recording defect or clerical error tied to the May filings. Instead, it purported to amend a mortgage that Whitefish Credit Union had already satisfied and expressly quitclaimed, with full knowledge of that release.

By that point, there was nothing pending to correct and no defect left unresolved. The only effect of the filing was to reopen ambiguity in a record the credit union had already cleared, transforming a finalized release into yet another revision of history.

Ruis Glacier, LLC

As the disputed paper trail continued to be treated as a live source of authority, Thornton took the step specifically designed by property law to prevent further quiet reshuffling of title: he recorded notices of lis pendens. The filings did not assert a new lien or revive a foreclosure.

Lis Pendens – Click Image Below

They served a narrower and more defensive purpose, to place the public on notice that the interests being claimed by Whitefish Credit Union and Ruis‑affiliated entities in the Somers property were actively contested and depended on instruments Thornton maintained had already been extinguished.

By recording the lis pendens, Thornton sought to freeze the status quo, ensuring that any future purchaser or lender would be alerted to the ongoing dispute rather than inheriting it unknowingly after yet another round of paperwork changed hands.

The practical effect of the lis pendens fell most heavily on Whitefish Credit Union, whose asserted interests sat at the center of the disputed chain of title. By recording the notice, Thornton ensured that any claim traced through Whitefish Credit Union, and by extension through Mo Somers and other downstream entities, could no longer be treated as settled or freely transferable without full awareness of the dispute.

The lis pendens did not invalidate recorded instruments or create a new lien, but it attached formal notice to the Somers property that constrained the credit union’s ability to rely on the Corrected Release as evidence of finality.

From that point forward, any lender, buyer, or title insurer examining the record would be alerted that Whitefish Credit Union’s claimed interest was under active challenge, preventing it from quietly leveraging, transferring, or repackaging that interest without confronting the underlying litigation.

Notably, none of the named entities sought to rebut or discharge the lis pendens after it was recorded.

That silence is striking given the resources and sophistication of the parties involved, particularly Whitefish Credit Union, a large institutional lender with ample legal capacity to challenge a notice it believed to be baseless or improper.

A lis pendens is not a subtle filing; it is designed to provoke response if the underlying claim is unfounded. The absence of any recorded challenge, motion to expunge, or corrective filing suggests that the entities relying on the Corrected Release were unwilling or unable to affirm its authority in a forum where it would be tested.

In that context, the lis pendens stands as more than a procedural notice. It operates as an unanswered objection, one that continues to speak precisely because no one with the means to contest it has done so.

The Reemergence of Glacier Bank

Glacier Bank reenters the narrative after almost 2 decades of absence not through litigation, but through the public land records. Having last appeared in connection with early loan activity predating Whitefish Credit Union’s involvement, Glacier Bank resurfaces as the recorded financing institution for the Silos development constructed by Ruis in downtown Kalispell.

Those records reflect a multi‑million‑dollar loan in which the contested Somers property is identified among the collateral securing the financing. The reappearance is notable not because of the Silos project itself, but because it links an unresolved and disputed parcel back into the banking system years after its title had become clouded by vacated judgments, extinguished liens, and corrective filings.

In that context, Glacier Bank’s role raises unavoidable questions about how a property so entangled in dispute could once again be treated as viable collateral in the ordinary course of commercial lending.

Where Things Go From Here

As of today, Dennis and Donna Thornton are simultaneously litigating against their adversaries in four separate courts: the United States Bankruptcy Court, the Montana Federal District Court, the Eleventh Judicial District Court in Kalispell, and the Ninth Circuit Court of Appeals. Remarkably, and perhaps without precedent in a case of this scope and duration, Thornton remains front and center in that fight as a pro se litigant, representing himself across multiple forums against well‑resourced institutional opponents.

It would be disingenuous, however, to portray Thornton as a lone wolf in this fight. While he has remained the central figure in the litigation, he has been supported by many people throughout the Flathead Valley who, after gaining an understanding of his case, chose to help in meaningful ways, something Thornton readily acknowledges.

In summary, the law is not ambiguous here. Under Montana’s own statutes and the basic principles affirmed repeatedly by federal courts, a vacated judgment and a dismissal with prejudice end the matter. Yet Thornton has spent nearly two decades fighting to make courts and institutions honor rules that are supposed to be automatic and nonnegotiable.

What should have concluded years ago has been prolonged through rulings and procedural maneuvers that contradict the controlling legal framework and keep Thornton locked in litigation while his property remains tied up. The result is not merely delay, but an ongoing deprivation of rights that Montana law says should already have been restored, and Thornton’s demand is as simple as it is overdue: apply the law as written, return what was taken, and hold accountable those who turned a settled dispute into a long running ordeal.

{kind=link}

{kind=link}

More Stories

Supreme Court Candidate May Face Judicial and Civil Complaints Based on Jurisdictional Ruling

Exclusive: Suspicious Hirings and Failure to Act Raise Questions About Montana AG Knudsen’s Connections to Flathead County Prosecutions

Video: NWLNews – Flathead County Organized Crime Update – 4.20.26